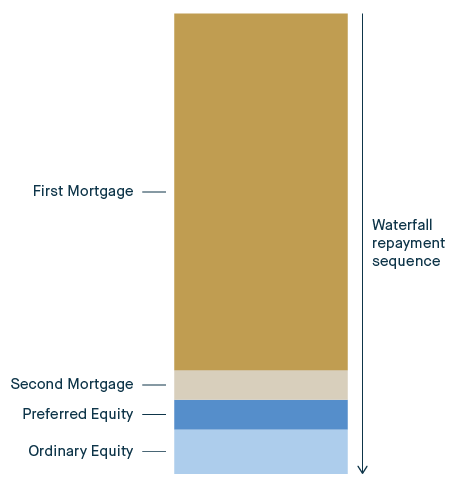

Depending on the nature, complexity, and location of an underlying CRE security property asset/project, there can be all kinds of variations within the capital stack. However, typically it consists of up to four funding sources or layers:

1. First Mortgage Debt

- Also referred to as ‘senior’ debt

- The primary funding source for a CRE development project/levered asset acquisition or investment

- Typically makes up the majority of the required capital

- First ranking mortgage security (usually registered) against the security property

- First in line in the repayment waterfall

- Buffered by equity (which is the ‘first loss position’) and other subordinated debt

- Least risk/lowest level of return, currently in the 6-8% per annum range

- Interest can be capitalised within the loan facility or paid along the way by the borrower

- Fixed (contractual) return with limited downside

2. Second Mortgage Debt

- Also referred to as ‘mezzanine’ or ‘junior’ debt

- Used as an additional layer of debt between First Mortgage Debt and Ordinary/Preferred Equity

- Second ranking mortgage security (also usually registered) against the security property

- Second in line in the repayment waterfall (i.e. First Mortgage Debt mortgagee must be repaid in full before any funds become available) and typically required to enter into a priority deed with the First Mortgage Debt mortgagee

- With higher risks, the holder demands a higher return, currently in the range of 12-14% per annum

- Interest can be capitalised within the loan facility or paid along the way by the borrower

- Fixed (contractual) return with limited downside

3. Preferred Equity

- A hybrid of debt and equity attributes

- Serves a similar function to Second Mortgage Debt in that an additional layer of capital exists between the debt holders and Ordinary Equity holders

- Secured contractually to the security property however, not by a registered mortgage instrument

- Third in line in the repayment waterfall

- In recognition of its unsecured nature, the investment may be structured with higher return and progressive coupon payments

- Returns are currently in the 14-16% per annum range, though may go higher with depending on level of ordinary equity participation

4. Ordinary Equity

- These are the unsecured funds the borrower invests; the capital that is ‘first in and last out’

- Required by the lender (e.g. Pallas Capital) to ensure the borrower has a strong, vested interest in the success of the CRE development project /asset acquisition or investment and so that the debt provider/s is/are not wholly exposed to any downside (i.e. ordinary equity is the ‘first loss position’ and provides the initial ‘buffer’ or ‘shock absorber’ to providers of debt/credit)

- The last layer of capital to be repaid in the repayment waterfall i.e. all Debt and Preferred Equity holders require full principal and interest repaid before Ordinary Equity receives any payment

- Highest risk-return in the capital stack, often the most profitable if the investment is successful (i.e. unlimited upside)

As shown in the diagram, below, these sources are ‘stacked’ on top of each other to fund the project (hence the name, capital stack):

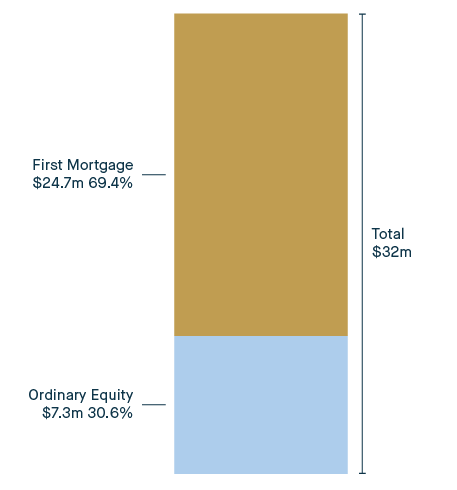

Case Study: No. 1 Carlisle, Rose Bay, NSW 2029

Pallas Capital is highly experienced in the principles and nuances of CRE structured finance (i.e. the capital stack). The recent Fortis development at No. 1 Carlisle St, Rose Bay, provides a good illustrative example. It’s worth noting that, for this project, only two of the four capital stack sources were required: First Mortgage Debt and Ordinary Equity, which is the most common capital structure used to fund a CRE project.

The Funding Scenario

To acquire the prominent Rose Bay site and subsequently deliver the boutique 8-residence development at No.1 Carlisle, the borrower/developer Fortis required $32 million in project capital. This was funded through a two-tiered capital structure. Pallas Capital provided $24.7 million in the form of First Mortgage Debt (equating to 69.4% of the total GRV-Gross Realisable Value). The remaining balance of $7.3 million was contributed directly by Fortis, as Ordinary Equity.

No.1 Carlisle – Capital Stack

| First Mortgage Debt: (Pallas Capital) | $24.7 million (69.4%) |

| Second Mortgage Debt: | n/a |

| Preferred Equity: | n/a |

| Ordinary Equity: (Fortis) | $7.3 million (30.6%) |

The Result

At the time of writing, No.1 Carlisle is in the final stages of completion. The eight luxury residences have already been 100% pre-sold during the construction phase, delivering Project Value on Completion of $40.1 million gross and $37 million net of GST (providing 150% debt cover on the First Mortgage Debt). Pallas Capital investors, as First Mortgage Unitholders, received an average return above 8.0% p.a. on their investment and Fortis as the Ordinary Equity holder (the developer) will realize a return of approx. 22% IRR on their investment.

No.1 Carlisle – Returns

| First Mortgage Debt: (Pallas Capital) | 8.0% coupon |

| Second Mortgage Debt: | n/a |

| Preferred Equity: | n/a |

| Ordinary Equity: (Fortis) | 22.0% IRR |

What if things go bad?

One of the key drivers of Pallas’ success is the way it manages its loan arrears and therefore its default rate.

Even by applying the most stringent underwriting processes, and by only lending to borrowers with the strongest of credit, very infrequently borrowers default on their loan obligations.

Where a borrower defaults, Pallas has a comprehensive default management plan, which can be summarised as follows:

- Identify – the first step is to advise the borrower of the default and request that it be rectified immediately and make payment of any costs incurred by Pallas arising from the default.

- Rectification Plan – if the borrower’s explanation for the default is reasonable and it is able to be rectified within 14 days, Pallas may agree arrangements for the borrower to cure the breach.

- Default Notices – if the default has not been rectified within 14 days, Pallas will then usually issue a default notice to the borrower and begin to apply penalty interest rates.

- Recovery Action – if the default has not been rectified within the time period stipulated in the default notice, Pallas will consult with its legal advisors to determine next steps, which may include exercising its rights to declare that the amount owing is immediately due for payment, make demands under guarantees and/or appoint a Receiver to take possession of, and secure the sale of, the security property.

- Enforcement of the Security – the Receiver will, as soon as practicable, typically obtain orders to obtain vacant possession of the security property and advertise the property for sale. The Receiver is obliged to take all reasonable care to sell the property for “not less than market value.” The Receiver will also take steps to enforce personal guarantees provided by the sponsors if the proceeds of the property sale are insufficient to repay the liabilities to Pallas.

- Loan Repayment – after payment of its fees, the Receiver will then pass on to Pallas the net proceeds of sale, which monies can then be used to repay the loan and all accrued interest and fees, including penalty interest.

The adoption of prudent lending criteria and, in particular, the use of conservative maximum LVRs calculated against a current independent property valuation means that the value of the underlying security property needs to fall by approximately 35% in the space of what is typically a 12-18 month loan term before investor capital is at risk, an outcome which has never occurred in relation to the Pallas loan book. Even in such a scenario, any shortfall could be expected to be resolved through the proceeds of a recovery action against the sponsor guarantees.